|

Nevada |

2834 |

95-4627685 |

|

(State

or Other Jurisdiction |

(Primary

Standard |

(IRS

Employer |

|

of

Incorporation |

Industrial

Classification "SIC" |

Identification

Number) |

|

or

Organization) |

Code

Number) |

|

Title

of Each Class of Securities to be Registered |

Number

of Shares to be Registered(1) (2) |

Proposed

Maximum

Offering

Price Per Share(1) (2) |

Proposed

Maximum

Aggregate

Offering Price |

Amount

of Registration Fee |

|||||||||

|

Shares

of Common Stock, $.001 par value |

481,557 |

$ |

2.20 |

$ |

1,059,425.40 |

$ |

124.69 |

||||||

|

Shares

of Common Stock, $.001 par value, underlying warrants and convertible

debentures(3) |

1,235,469 |

$ |

2.20 |

$ |

2.718,031.80 |

$ |

319.91 |

||||||

|

TOTAL |

1,717,026 |

$ |

3,777,457.20 |

$ |

444.60 |

||||||||

|

(1) |

Estimated

solely for the purpose of calculating the amount of the registration fee

pursuant to Rule 457(c). |

|

(2) |

Pursuant

to Rule 416 under the Securities Act of 1933, as amended, there are also

being registered such additional shares of common stock as may become

issuable pursuant to anti-dilution provisions of the

warrants. |

|

(3) |

590,308

of the shares are issuable upon exercise of the warrants and 645,161 of

the shares upon conversion of the convertible

debentures |

|

SPECIAL

NOTE REGARDING FORWARD LOOKING STATEMENTS |

1 |

|

PROSPECTUS

SUMMARY |

1 |

|

RISK

FACTORS |

4 |

|

USE

OF PROCEEDS |

8 |

|

SELLING

STOCKHOLDERS |

9 |

|

PLAN

OF DISTRIBUTION |

11 |

|

LEGAL

PROCEEDINGS |

13 |

|

DIRECTORS,

EXECUTIVE OFFICERS, PROMOTERS AND CONTROL PERSONS |

14 |

|

SECURITY

OWNERSHIP OF CERTAIN BENEFICIAL OWNERS AND

MANAGEMENT |

16 |

|

DESCRIPTION

OF SECURITIES |

17 |

|

DISCLOSURE

OF COMMISSION POSITION OF INDEMNIFICATION FOR SECURITIES ACT

LIABILITIES |

17 |

|

DESCRIPTION

OF BUSINESS |

18 |

|

MANAGEMENT’S

DISCUSSION AND ANALYSIS AND PLAN OF OPERATIONS |

30 |

|

DESCRIPTION

OF PROPERTY |

51 |

|

CERTAIN

RELATIONSHIPS AND RELATED TRANSACTIONS |

51 |

|

MARKET

FOR COMMON EQUITY AND RELATED STOCKHOLDER MATTERS |

53 |

|

EXECUTIVE

COMPENSATION |

53 |

|

CHANGES

IN AND DISAGREEMENTS WITH ACCOUNTANTS ON ACCOUNTING AND FINANCIAL

DISCLOSURE |

57 |

|

WHERE

YOU CAN FIND MORE INFORMATION |

57 |

|

FINANCIAL

STATEMENTS |

F-1 |

|

EXHIBITS |

63 |

|

UNDERTAKING |

64 |

|

Common

Stock Offered |

This

prospectus relates to the offering of 1,717,026 shares of our common

stock, which may be sold from time to time by the selling stockholders

named in this prospectus. Of the total amount offered, 645,161 shares of

common stock are issuable upon the conversion of convertible debentures

sold by NetSol in a private placement in March 2004 and 322,581 shares of

common stock are issuable to such selling stockholders upon the exercise

of warrants issued in connection with that placement; 386,362 shares of

common stock were issued in a private placement which closed in May 2004,

and 193,182 shares of common stock are issuable to the selling

stockholders upon the exercise of warrants issued in connection with the

private placement. Maxim Group LLC served as NetSol’s placement agent in

connection with such private placements and, its nominee, Maxim Partners,

was issued warrants to purchase up to 74,545 shares of common stock in

connection with their services. 50,000 shares of common stock were

acquired by an individual non-U.S. resident investor in exchange for the

payment of a tax liability owed by our Pakistani subsidiary. 45,195 shares

of common stock were acquired by a selling stockholder in a settlement

agreement between NetSol and the selling stockholder entered into in

October 2003. The shares of our common stock are being registered to

permit the selling stockholders to sell the shares from time to time in

the public market. The selling stockholders will determine the timing and

amount of any sale. |

|

Common

Stock outstanding |

We

had 13,707,547 shares of common stock issued and outstanding as of

May

25, 2005. |

|

Use

of Proceeds |

We

will not receive any of the proceeds from sale of shares of common stock

offered by the selling stockholders. |

|

Trading

Market |

Our

common stock is currently listed on the NASDAQ SmallCap Market under the

trading symbol “NTWK.” |

|

Risk

Factors |

Investment

in our common stock involves a high degree of risk. You

should carefully consider the information set forth in the "Risk Factors"

section of this prospectus as well as other information set forth in this

prospectus, including our financial statements and related

notes. |

|

• |

political

uncertainty in Pakistan and the Southeast Asian Region, particularly in

light of the United States’ war on terrorism and the Iraq

war; |

| • | recessions in foreign countries; |

|

• |

fluctuations

in currency exchange rates, particularly the weakness of the U.S. dollar

and the effect this may have on U.S. off-shore technology

spending; |

| • | difficulties and costs of staffing and managing foreign operations; |

| • | reduced protection for intellectual property in some countries; |

|

• |

political

instability or changes in regulatory requirements or the potential

overthrowing of the current government in certain foreign countries;

|

|

• |

U.S.

imposed restrictions on the import and export of technologies;

and, |

|

• |

U.S.

imposed restrictions on the issuances of business and travel visas to

foreign workers primarily those from Middle Eastern or East Asian

countries. |

|

• |

our

ability to integrate strategy, experience modeling, creative design and

technology services; |

| • | quality of service, speed of delivery and price; |

| • | industry knowledge; |

| • | sophisticated project and program management capability; and, |

| • | Internet technology expertise and talent. |

| • | ability of our competitors to hire, retain and motivate professional staff; |

|

• |

development

by others of Internet services or software that is competitive with our

solutions; and |

| • | extent of our competitors’ responsiveness to client needs. |

|

• |

quarterly

variations in operating results and achievement of key business

metrics; |

| • | changes in earnings estimates by securities analysts, if any; |

|

• |

any

differences between reported results and securities analysts’ published or

unpublished expectations; |

|

• |

announcements

of new contracts or service offerings by NetSol or

competitors; |

|

• |

market

reaction to any acquisitions, joint ventures or strategic investments

announced by NetSol or competitors; |

|

• |

demand

for our services and products; |

|

• |

changes

of shares being sold pursuant to Rule 144 or upon exercise of the

warrants; and, |

|

• |

general

economic or stock market conditions unrelated to NetSol’s operating

performance. |

|

Name

of Selling Stockholder(1) |

Number

of Shares of

NetSol

Common Stock

Beneficially

Owned Prior

to

the Offering(1) |

Number

of Shares of

NetSol

Common Stock Being Offered Hereby (1) |

Number

of Shares of

NetSol

Common Stock to be

Beneficially

Owned Upon Completion of the Offering(1)(2) |

|||||||

|

Maxim

Partners, LLC (3) |

155,545 |

74,545 |

0 |

|||||||

|

Natalie

L. Khur Revocable Trust(4) |

78,410(4 |

) |

78,410 |

0 |

||||||

|

Richard

E. Kent & Lara T. Kent |

285,190(5 |

) |

285,190 |

0 |

||||||

|

Alfonse

M. D’Amato Defined Benefit Plan(6) |

148,826(6 |

) |

148,826 |

0 |

||||||

|

Jay

Youngerman & Toni Youngerman |

40,908(7 |

) |

40,908 |

0 |

||||||

|

Girish

C Shah IRA (8) |

34,090(9 |

) |

34,090 |

0 |

||||||

|

Douglas

Friedenberg IRA Standard/SEP DTD 04/16/01(10) |

34,090(9 |

) |

34,090 |

0 |

||||||

|

Fred

Arena |

34,090(9 |

) |

34,090 |

0 |

||||||

|

Grossman

Family Trust (11) |

51,136(11 |

) |

51,136 |

0 |

||||||

|

Hugh

Brook |

34,090(9 |

) |

34,090 |

0 |

||||||

|

Michael

K. Harley |

40,323(12 |

) |

40,323 |

0 |

||||||

|

W.

R. Savey |

40,323(12 |

) |

40,323 |

0 |

||||||

|

Robert

Stranczek |

40,323(12 |

) |

40,323 |

0 |

||||||

|

The

Viney Settlement Number 1 (13) |

120,967(13 |

) |

120,967 |

0 |

||||||

|

Ronald

K. Marks |

40,323(12 |

) |

40,323 |

0 |

||||||

|

Leonard

Carinci |

40,323(12 |

) |

40,323 |

0 |

||||||

|

Peter

J. Jegou(14) |

40,323(12 |

) |

40,323 |

0 |

||||||

|

Joseph

Marotta & Nancy J. Marotta |

40,323(12 |

) |

40,323 |

0 |

||||||

|

D.G.

Fountain |

40,323(12 |

) |

40,323 |

0 |

||||||

|

Lee

A. Pearlmutter Revocable Trust U/A dated 10/9/92 as amended 2/28/96

(15) |

40,323(12 |

) |

40,323 |

0 |

||||||

|

Wayne

Saker |

40,323(12 |

) |

40,323 |

0 |

||||||

|

Donald

Asher Family Trust dated 7/11/01 (16) |

40,323(12 |

) |

40,323 |

0 |

||||||

|

Jeffrey

Grodko |

40,323(12 |

) |

40,323 |

0 |

||||||

|

Emeric

R. Holderith |

20,161(17 |

) |

20,161 |

0 |

||||||

|

John

O’Neal Johnston trust u/a DTD 5/17/93 (18) |

20,161(17 |

) |

20,161 |

0 |

||||||

|

Judith

Barclay |

40,323(12 |

) |

40,106 |

0 |

||||||

|

Allen

W. Coburn & Maureen B. Coburn |

20,161(17 |

) |

20,161 |

0 |

||||||

|

John

C. Moss |

20,161(17 |

) |

20,161 |

0 |

||||||

|

Landing

Wholesale Group Defined Benefit Plan(19) |

40,323(12 |

) |

40,323 |

0 |

||||||

|

Jerold

Weigner & Lilli Weigner |

40,323(12 |

) |

40,323 |

0 |

||||||

|

Mohammed

Iqbal |

50,000(20 |

) |

50,000 |

0 |

||||||

|

ACB

Ltd.(21) |

45,195(21 |

) |

45,195 |

0 |

||||||

|

TOTAL |

1,798,026 |

1,717,026 |

0 |

| (1) |

Beneficial

ownership is determined in accordance with the rules of the Securities and

Exchange Commission and generally includes voting or investment power with

respect to such securities. |

| (2) |

None

of the Selling Stockholders has held an employment, officer or director

position with NetSol within the past three years. Assuming that all shares

being registered hereby will be sold, all debentures will be converted and

all warrants will be exercised, no selling stockholder will hold a

percentage interest in the shares of NetSol in excess of 1 percent at the

completion of the offering. |

| (3) |

Maxim

Partners LLC owns 98% of Maxim Group LLC, a registered broker dealer. MJR

Holdings LLC owns 72% of Maxim Partners LLC. Mike Rabinowitz is the

principal manager of MJR Holdings and has principal voting and dispositive

power with respect to the securities owned by Maxim Partners LLC. The

number of shares beneficially owned include 74,545 warrants to acquire

common stock which are being registered hereby and warrants to acquire

81,000 shares of common stock previously registered which were issued as

compensation to Maxim Partners, as nominee of Maxim Group, for services

provided to NetSol in its July 2003 private

placement. |

| (4) |

Adam

Kuhr, as trustee, is the beneficial owner of the Natalie L. Kuhr Revocable

Trust. The shares of common stock consist of 52,273 shares of common stock

and 26,137 shares of common stock underlying warrants acquired in the May

2004 placement. |

| (5) |

Consisting

of 190,127 shares of common stock of which 136,364 shares were acquired in

the May 2004 placement and 53,763 shares issuable upon conversion of the

principal dollar amount of its convertible debenture; and, 95,063 shares

of common stock underlying warrants of which 68,182 are shares of common

stock underlying warrants issued in the May 2004 placement and 26,881 are

shares of common stock underlying warrants issued in connection with the

March 2004 private placement of convertible

debentures. |

| (6) |

Alfonse

M. D’Amato is the beneficial owner of the Alfonse M. D’Amato Defined

Benefit plan. The shares of common stock consist of 99,217 shares of

common stock of which 45,454 shares were acquired in the May 2004

placement and 53,763 shares are issuable upon conversion of the principal

dollar amount of its convertible debenture; and, 49,609 shares of common

stock underlying warrants of which 22,727 shares of common stock underly

warrants issued in the May 2004 placement and 26,882 are shares of common

stock underlying warrants issued in connection with the March 2004 private

placement of convertible debentures. |

| (7) |

Consisting

of 27,272 shares of common stock and 13,636 shares of common stock

underlying warrants acquired in the May 2004 private

placement. |

| (8) |

Girish

C. Shah is the beneficial owner of the Girish C. Shah

IRA. |

| (9) |

Consisting

of 22,727 shares of common stock and 11,363 shares of common stock

underlying warrants acquired in the May 2004 private

placement. |

| (10) |

Douglas

Friedenberg is the beneficial owner of the Douglas Friedenberg IRA

Standard/SEP DTE 04/16/01. |

| (11) |

Raphael

Z. Grossman, as trustee, is the beneficial owner of the Grossman Family

Trust. The shares of common stock consist of 34,091 shares of common stock

and 17,045 shares of common stock underlying warrants acquired in the May

2004 private placement. |

| (12) |

Consisting

of 26,882 shares of common stock issuable upon conversion of the principal

dollar amount of its debenture and 13,441 shares of common stock

underlying warrants issued in connection with the March 2004 placement of

convertible debentures. |

| (13) |

John

Viney, as trustee, is the beneficial owner of the Viney Settlement Number

1. Shares of common stock consist of 80,645 shares of common stock

issuable upon the conversion of the principal dollar amount of its

debenture and 40,332 shares of common stock underlying warrants issued in

connection with the March 2004 placement of convertible

debentures. |

| (14) |

Peter

J. Jegou is the beneficial holder of 26,882 shares issuable upon the

conversion of the principal dollar amount of his convertible debenture and

13,441 shares underlying warrants issued in connection with the March 2004

placement of convertible debentures. |

| (15) |

Lee

A. Pearlmutter, as trustee, is the beneficial owner of the Lee A.

Pearlmutter Revocable Trust dated 10/9/92 as Amended 2/28/96.

|

| (16) |

D.S.

Asher, as trustee, is the beneficial owner of the Donald Asher Family

Trust. |

| (17) |

Consisting

of 13,441 shares issuable upon conversion of the principal dollar amount

of its convertible debenture and 6,720 shares underlying warrants issued

in connection with the March 2004 placement of convertible

debentures. |

| (18) |

John

O’Neal Johnston, as trustee, is the beneficial owner of the John O’Neal

Johnston Trust U/A DTD 05/17/93. |

| (19) |

Andrew

Bellow Jr. is the beneficial owner of the Landing Wholesale Group Defined

Benefit Plan. |

| (20) |

Mr.

Iqbal received his shares in a share purchase agreement whereby he

received 50,000 shares in exchange for satisfying a tax liability of

NetSol’s Pakistani subsidiary. This agreement required NetSol to register

the shares of common stock in this

offering. |

| (21) |

Tony

De Nazareth, as managing director, is the beneficial owner of ACB

Ltd. |

|

• |

purchases

by a broker-dealer as principal and resale by the broker-dealer for its

own account pursuant to this prospectus; |

|

• |

ordinary

brokerage transactions and transactions in which the broker solicits

purchasers; |

|

• |

block

trades in which the broker-dealer so engaged will attempt to sell the

securities as agent but may position and resell a portion of the block as

principal to facilitate the transaction; |

|

• |

an

over-the-counter sale; |

|

• |

in

privately negotiated transactions; and, |

|

• |

in

options transactions. |

|

Name |

Year

First Elected As an Officer

Or

Director |

Age |

Position

Held with the Registrant |

Family

Relationship | ||||

|

Najeeb

Ghauri |

1997 |

51 |

Chief

Financial Officer, Director and Chairman |

Brother

to Naeem and Salim Ghauri | ||||

|

Salim

Ghauri |

1999 |

49 |

President

and Director |

Brother

to Naeem and Najeeb Ghauri | ||||

|

Naeem

Ghauri |

1999 |

47 |

Chief

Executive Officer and Director |

Brother

to Najeeb and Salim Ghauri | ||||

|

Patti

L. W. McGlasson |

2004 |

39 |

Secretary |

None | ||||

|

Shahid

Javed Burki |

2000 |

65 |

Director

|

None | ||||

|

Eugen

Beckert |

2001 |

58 |

Director |

None | ||||

|

Jim

Moody |

2001 |

68 |

Director |

None | ||||

|

Derek

Soper |

2005 |

67 |

Director |

None |

Percentage |

|||||||

Number

of |

Beneficially |

||||||

|

Name

and

Address |

Shares(1)(2) |

owned(3) |

|||||

|

Najeeb

Ghauri (4) |

912,650 |

6.66 |

% | ||||

|

Naeem

Ghauri (4) |

761,367 |

5.55 |

% | ||||

|

Salim

Ghauri (4) |

877,416 |

6.51 |

% | ||||

|

Jim

Moody (4) |

87,000 |

* |

|||||

|

Eugen

Beckert (4) |

179,000 |

1.31 |

% | ||||

|

Shahid

Javed Burki (4) |

93,000 |

* |

|||||

|

Derek

Soper(4) |

100,000 |

* |

|||||

|

Patti

L. W. McGlasson (4) |

75,000 |

* |

|||||

|

All

officers and directors as a group (nine persons) |

3,085,433 |

22.51

|

% | ||||

| * | Less than one percent |

| (1) | Except as otherwise indicated, NetSol believes that the beneficial owners of the common stock listed in this table, based on information furnished by such owners, have sole investment and voting power with respect to such shares, subject to community property laws where applicable. Beneficial ownership is determined in accordance with the rules of the Securities and Exchange Commission and generally includes voting or investment power with respect to securities. |

| (2) | Beneficial ownership is determined in accordance with the rules of the Commission and generally includes voting or investment power with respect to securities. Shares of common stock relating to options currently exercisable or exercisable within 60 days of May 25, 2005 are deemed outstanding for computing the percentage of the person holding such securities but are not deemed outstanding for computing the percentage of any other person. Except as indicated by footnote, and subject to community property laws where applicable, the persons named in the table above have sole voting and investment power with respect to all shares shown as beneficially owned by them. |

| (3) | Percentage ownership is based on 13,707,547 shares issued and outstanding at May 25, 2005. |

| (4) | Address c/o NetSol Technologies, Inc. at 23901 Calabasas Road, Suite 2072, Calabasas, CA 91302. |

|

2004 |

2003 |

||||||

|

North

American (NetSol USA) |

12 |

% |

15 |

% | |||

|

Europe

(NetSol Technologies, UK Ltd.) |

6 |

% |

5 |

% | |||

|

Other

International (Abraxas, NetSol Technologies Pvt. Ltd., |

82 |

% |

80 |

% | |||

|

NetSol

Pvt., Ltd., NetSol Connect) |

|||||||

|

Total

Revenues |

100 |

% |

100 |

% | |||

| · |

Software

Process Improvement Services for NADRA. (National Database Registration

Authority of Pakistan) |

| · |

MM

Training Workshops as consultants for PSEB (Pakistan Software Export Board

). |

| · |

Credit

MIS & FIS for PRSP (Punjab Rural Support

Program) |

| · |

Electronic

Credit Information Bureau for State Bank of

Pakistan |

| · |

Punjab

Portal |

| · |

Consultancy

& Automation of Pakistan Administrative Staff

College |

| · |

Pakistan

Administrative Staff College |

| · |

Punjab

Portal Government of Punjab |

| · |

Punjab

Rural Support Program |

| · |

Pakistan

Software Export Board |

| · |

NADRA |

| · |

Pakistan

Air War College |

| · |

State

Bank of Pakistan |

| · |

Achieve

CMM Level 5 Accreditation in 2005. |

| · |

Enhance

Software Design, Engineering and Service Delivery Capabilities by

increasing investment in training. |

| · |

Enhance

and invest in R&D or between 5-7% of yearly budgets in financial,

banking and various other domains within NetSol’s core

competencies. |

| · |

Continue

recruiting additional senior level marketing and technical professionals

in Lahore, London, and Adelaide offices to be able to support potential

new customers from the North American and European

markets. |

| · |

Recruit

senior marketing and sales executives to oversee the global marketing

operations. |

| · |

In

June 2004, the Company relocated its entire staff in Lahore to three

floors of its newly built, fully dedicated and wholly owned Technology

Campus. The Company is in the process of expanding the last two remaining

floors to add new personnel. |

| · |

Increase

Capex, to enhance Communications and Development Infrastructure. Roll out

a second phase of construction of technology Campus in Lahore to respond

to a growth of new orders and customers. |

| · |

Launch

new business development initiatives for various products and services

such as LeaseSoft in hyper growth economies such as

China. |

| · |

Appoint

a senior marketing executive from CQ systems to head up new initiatives in

China. |

| · |

Create

new technology partnership with Oracle and strengthen our relationship

with Intel in Asia Pacific and in the USA. |

| · |

Aggressive

marketing strategy in local government and private sectors in Pakistan.

Participate in biggest and largest value IT projects in the public sectors

of government of Pakistan. |

| · |

Ramping

up the telecom sectors through its majority owned subsidiary NetSol Akhter

and injecting needed capital. The telecom sector is one of the most

untouched sectors in Pakistan. NetSol has seized this opportunity to

aggressively market its products and services with its strong

infrastructure, brand name and resources in this

region. |

| · |

Aggressive

new business development activities in UK and European markets through

organic growth, new alliances and mergers and

acquisition. |

| · |

Explore

new and diversify into Business Processing Outsourcing (“BPO”) areas due

to explosive outsourcing into offshore

model. |

| · |

Launch

LeaseSoft into new markets by assigning new, well established companies as

distributors in Europe, Asia Pacific including

Japan. |

| · |

Expand

relationships with key customers in the US, Europe and Asia

Pacific. |

| · |

Expand

global sales opportunities with existing customers such as DaimlerChrysler

Group, Toyota Leasing and, Yamaha Motors. |

| · |

Enhance

pricing of LeaseSoft products based on its demand and

growth. |

| · |

Product

Positioning through alliances, joint ventures and

partnerships. |

| · |

Direct

Marketing of Services. |

| · |

Embark

on roll up strategy by broadening M&A activities broadly in the

software development domain. |

| · |

Aggressively

pursue software companies in the US and in Europe to launch a strong

foothold in these markets. |

| · |

Effectively

position and marketing campaign for InBanking system. This is a

potentially big revenue generator in the banking domain for which NetSol

has already invested significant time and resources towards completing the

development of this application. Seeking major development partners to

market this treasury system in the global

markets. |

| · |

The

Company’s current positive cash flow based primarily on the addition of CQ

Systems and continued organic growth. The Company’s aim is to continue to

further strengthen the balance sheet and cash reserves in order to attract

large customers world wide. |

| · |

The

Company continues to explore various means and most cost efficient methods

to inject new capital for the growth it is experiencing. With this in

mind, and pursuant to an agreement with AKD Securities, the Company has

proceeded with the IPO of the shares of common stock of NetSol

Technologies Ltd., its subsidiary located in Lahore, Pakistan on the

Karachi Stock Exchange (KSE). Over $1.5 million was raised in the pre-IPO

private placement which will be followed by the Initial Public Offering

which is anticipated to raise approximately $4.5 million.

|

| · |

Infuse

new capital from potential exercise of outstanding investor warrants and

employees options for business development and enhancement of

infrastructures. |

| · |

NetSol

has engaged Westrock Advisors LLC, in New York for new investor relations

and company coverage. |

| · |

NetSol’s

continued profitability has permitted the Company to develop opportunities

to introduce the Company to small cap funds and institutions in the U.S.

Market. This effort is assisted and coordinated by its investment advisor,

Maxim Group LLC, our investor relations consultant, McCloud Communications

and, newly hired consultants, SGI

International. |

| · |

Continue

to review costs at every level and take appropriate steps to further

reduce operating overheads. |

| · |

Discontinue

any programs, projects or offices that are not producing desirable and

positive results |

| · |

Consistently

improving quality standards and work to achieve CMMi Level 5 standard by

sometime in 2006 |

| · |

Grow

process automation. |

| · |

Profit

Centric Management Incentives. |

| · |

More

local empowerment and P&L Ownership in each Country

Office. |

| · |

Improve

productivity at the development facility and business development

activities. |

| · |

Cost

efficient management of every operation and continue further consolidation

to improve bottom line. |

| · |

Improve

prices of all our product offerings, yet maintain the competitiveness.

This will further improve gross margins across the

board. |

| · |

Further

consolidating the subsidiaries by combining and integrating operating

units. |

| · |

Effectively

and efficiently integrate both back end and front end operations of CQ

Systems with NetSol. This would improve margins, reduce fixed costs of

developments and simply introduce newer cost efficiencies based on both

companies strengths of processes and good business

practices. |

| · |

Outsourcing

of services and software development is growing

worldwide. |

| · |

The

Global IT budgets are estimated to exceed $1.2 trillion in 2004, according

to the internal estimates of Intel Corporation. About 50% of this IT

budget would be consumed in the U.S. market alone primarily on the people

and processes. |

| · |

Burgeoning

Chinese markets, Asian markets in general and economic

boom. |

| · |

Overall

economic expansion worldwide and explosive growth in the merging markets

specifically. |

| · |

Regional

stability and improving political environment between Pakistan and

India. |

| · |

Economic

turnaround in Pakistan including: a steady increase in gross domestic

product; much stronger dollar reserves, which is at an all time high of

over $13 billion; stabilizing reforms of government and financial

institutions; improved credit ratings in the western markets, and strong

stock markets. |

| · |

Pakistan’s

continuous fight against extremism and terrorism in the region, boosting

confidence of foreign investors and

companies. |

| · |

Major

turnarounds in the telecom sector as new opportunities are arising due to

privatization, new incentives, reduction of bandwidth prices and

tariffs. |

| · |

The

stability in economic, political and business fronts in Pakistan has

opened numerous new opportunities particularly in the telecom and private

sectors. |

| · |

Steady

increase in foreign direct investments in Pakistan and new entry of many

large technology companies in Pakistan. |

| · |

The

disturbance in Middle East and rising terrorist activities post 9/11

worldwide have resulted in issuance of travel advisory in some of the most

opportunistic markets. In addition, travel restrictions and new

immigration laws provide delays and limitations on business travel.

|

| · |

The

potential impact of higher U.S. interest rates including, but not limited

to, fear of inflation that may drive down IT budgets and spending by U.S.

companies. |

| · |

Higher

oil prices worldwide may slow down the global economy causing delays in

new orders and reduction in budges. |

|

NETSOL

TECHNOLOGIES INC AND SUBSIDIARIES | ||||||||

|

CONSOLIDATED

PRO-FORMA STATEMENT OF FINANCIAL CONDITIONS | ||||||||

|

FOR

THE PERIOD ENDED JUNE 30, 2004 | ||||||||

|

(UNAUDITED)

|

|

NetSol

|

CQ

Systems |

|||||||||||||||

|

as

of 6/30/04 |

as

of 3/31/04 |

Pro

Forma |

Pro

Forma |

|||||||||||||

|

(Historical)

|

(Historical)

|

Adjustment

|

Combined

|

|||||||||||||

|

ASSETS |

||||||||||||||||

|

Current

Assets |

$ |

3,563,501 |

$ |

2,337,549 |

$ |

(700,000 |

) |

(1 |

) |

$ |

5,201,050 |

|||||

|

Property

& equipment, net |

4,203,580

|

260,517

|

-- |

4,464,097

|

||||||||||||

|

Intangible

assets, net |

4,218,040

|

-- |

5,809,020

|

(1 |

) |

10,027,060

|

||||||||||

|

Total

assets |

$ |

11,985,121 |

$ |

2,598,066 |

$ |

5,109,020 |

$ |

19,692,207 |

||||||||

|

|

||||||||||||||||

|

LIABILITIES

& STOCKHOLDERS' EQUITY |

||||||||||||||||

|

Current

liabilities |

$ |

3,573,948 |

$ |

1,600,914 |

$ |

-- |

$ |

5,174,862 |

||||||||

|

Obligations

under capitalized leases, |

||||||||||||||||

|

less

current maturities |

27,604

|

70,424

|

--

|

98,028

|

||||||||||||

|

Deferred

tax |

--

|

5,366

|

--

|

5,366

|

||||||||||||

|

Notes

payable |

89,656

|

--

|

4,353,587

|

(1 |

) |

4,443,242

|

||||||||||

|

Convertible

debenture |

937,500

|

--

|

--

|

937,500

|

||||||||||||

|

Total

liabilities |

4,628,708

|

1,676,704

|

4,353,587

|

10,658,998

|

||||||||||||

|

Stockholders'

equity; |

||||||||||||||||

|

Common

stock |

9,483

|

159,210

|

(158,528 |

) |

(1 |

) |

10,165

|

|||||||||

|

Additional

paid in capital |

38,933,621

|

--

|

1,676,113

|

(1 |

) |

40,609,734

|

||||||||||

|

Stock

subscription receivable |

(497,559 |

) |

--

|

--

|

(497,559 |

) | ||||||||||

|

Treasury

stock |

(21,457 |

) |

--

|

--

|

(21,457 |

) | ||||||||||

|

Other

comprehensive income (loss) |

(150,210 |

) |

138,784

|

(138,784 |

) |

(1 |

) |

(150,210 |

) | |||||||

|

Accumulated

earnings (deficit) |

(30,917,465 |

) |

623,368

|

(623,368 |

) |

(1 |

) |

(30,917,465 |

) | |||||||

|

Total

stockholders' equity |

7,356,413

|

921,362

|

755,433

|

9,033,208

|

||||||||||||

|

Total

liabilities and stockholders' equity |

$ |

11,985,121 |

$ |

2,598,066 |

$ |

5,109,020 |

$ |

19,692,206 |

||||||||

|

NOTES:

|

| (1) | Elimination of Common stock and accumulated earnings of CQ Systems before the acquisition and to record the purchase of CQ Systems by NetSol. The initial purchase price is $6,730,382, of which one-half is due at closing in cash and stock and the remaining half to be paid within one year, and after the price has been adjusted up or down when the audited 3/31/06 numbers are available. No interest is accrued on the balance remaining after closing. |

|

Purchase

Price allocation: |

$ |

||||||

|

Common

Stock, 681,965 shares |

682

|

||||||

|

Additional

paid in capital |

1,676,113

|

||||||

|

Cash

|

700,000

|

||||||

|

Cash,

provided by short-term notes |

1,000,000

|

||||||

|

Notes

payable |

3,353,587

|

||||||

|

Total

purchase price |

6,730,382

|

||||||

|

CQ

equity (net assets and liabilities) |

921,362

|

||||||

|

Intangible

assets: |

|||||||

|

Customer

Lists |

1,316,880

|

||||||

|

Licenses

|

2,190,807

|

||||||

|

Goodwill

|

2,301,333

|

||||||

|

5,809,020

|

5,809,020

|

||||||

|

6,730,382

|

|||||||

|

NETSOL

TECHNOLOGIES INC AND SUBSIDIARIES | ||||||||

|

CONSOLIDATED

PRO-FORMA STATEMENT OF OPERATIONS | ||||||||

|

FOR

THE YEAR ENDED JUNE 30, 2004 | ||||||||

|

(UNAUDITED) |

|

NetSol |

CQ

Systems |

|||||||||||||||

|

as

of 6/30/04 |

as

of 3/31/04 |

Pro

Forma |

Pro

Forma |

|||||||||||||

|

(Historical) |

(Historical) |

Adjustment |

Combined |

|||||||||||||

|

Net

Revenue |

$ |

5,749,062 |

$ |

4,640,653 |

$ |

-- |

$ |

10,389,715 |

||||||||

|

Cost

of revenue |

2,656,377

|

1,833,994

|

--

|

4,490,371

|

||||||||||||

|

Gross

profit |

3,092,685

|

2,806,659

|

--

|

5,899,344

|

||||||||||||

|

Operating

expenses |

6,028,055

|

1,895,988

|

701,537

|

(3 |

) |

8,625,577

|

||||||||||

|

Income

(loss) from operations |

(2,935,370 |

) |

910,671

|

(701,537 |

) |

(2,726,233 |

) | |||||||||

|

Other

income and (expenses) |

(307,764 |

) |

(214,819 |

) |

--

|

(522,583 |

) | |||||||||

|

Income

(loss) from continuing operations |

(3,243,134 |

) |

695,852

|

(701,537 |

) |

(3,248,816 |

) | |||||||||

|

Minority

interest in subsidiary |

273,159

|

--

|

--

|

273,159

|

||||||||||||

|

Net

income (loss) |

(2,969,975 |

) |

695,852

|

(701,537 |

) |

(2,975,657 |

) | |||||||||

|

Other

comprehensive income (loss): |

||||||||||||||||

|

Translation

adjustment |

(299,507 |

) |

110,837

|

--

|

(188,670 |

) | ||||||||||

|

Comprehensive

income (loss) |

$ |

(3,269,482 |

) |

$ |

806,689 |

$ |

(701,537 |

) |

$ |

(3,164,327 |

) | |||||

|

EARNINGS

PER SHARE |

||||||||||||||||

| Weighted -average number of shares outstanding |

8,563,518

|

100,000

|

8,663,518

|

|||||||||||||

|

Income

(loss) per share |

$ |

(0.35 |

) |

$ |

6.96 |

$ |

(0.34 |

) | ||||||||

|

NOTES: |

| (1) | Loss per share data shown above are applicable for both primary and fully diluted. |

| (2) | Weighted-average number of shares outstanding for the combined entity includes all shares issued for the acquisition of 681,964 shares as if outstanding as of July 1, 2003. |

| (3) | Amortization of intangible assets acquired in acquisition |

|

NETSOL

TECHNOLOGIES INC AND SUBSIDIARIES | ||||||||

|

CONSOLIDATED

PRO-FORMA STATEMENT OF FINANCIAL CONDITIONS | ||||||||

|

FOR

THE PERIOD ENDED JUNE 30, 2003 | ||||||||

|

(UNAUDITED) |

|

NetSol

|

CQ

Systems |

||||||||||||||||||

|

as

of 6/30/03 |

as

of 3/31/03 |

Pro

Forma |

Pro

Forma |

||||||||||||||||

|

(Historical)

|

(Historical)

|

Adjustment

|

Combined

|

||||||||||||||||

|

ASSETS |

|||||||||||||||||||

|

Current

Assets |

$ |

1,774,553 |

$ |

1,470,485 |

$ |

(700,000 |

) |

$ |

2,545,038 |

||||||||||

|

Property

& equipment, net |

2,037,507

|

197,481

|

--

|

2,234,988

|

|||||||||||||||

|

Intangible

assets, net |

4,930,191

|

--

|

6,212,409

|

(1 |

) |

11,142,599

|

|||||||||||||

|

Total

assets |

$ |

8,742,251 |

$ |

1,667,966 |

$ |

5,512,409 |

$ |

15,922,625 |

|||||||||||

|

LIABILITIES

& STOCKHOLDERS' EQUITY |

|||||||||||||||||||

|

Current

liabilities |

$ |

3,533,614 |

$ |

1,139,770 |

$ |

-- |

$ |

4,673,384 |

|||||||||||

| Obligations under capitalized leases, less current maturities |

7,111

|

8,330

|

15,441

|

||||||||||||||||

|

Deferred

tax |

--

|

1,892

|

1,892

|

||||||||||||||||

|

Notes

payable |

126,674

|

--

|

4,353,587

|

(1 |

) |

4,480,260

|

|||||||||||||

|

Total

liabilities |

3,667,399

|

1,149,992

|

4,353,587

|

9,170,977

|

|||||||||||||||

|

Stockholders'

equity; |

|||||||||||||||||||

|

Common

stock |

5,757

|

159,210

|

(158,528 |

) |

(1 |

) |

6,439

|

||||||||||||

|

Additional

paid in capital |

33,409,953

|

--

|

1,676,113

|

(1 |

) |

35,086,066

|

|||||||||||||

|

Stock

subscription receivable |

(84,900 |

) |

(84,900 |

) | |||||||||||||||

|

Other

comprehensive income (loss) |

149,297

|

27,947

|

(27,947 |

) |

(1 |

) |

149,297

|

||||||||||||

|

Accumulated

earnings (deficit) |

(28,405,255 |

) |

330,816

|

(330,816 |

) |

(1 |

) |

(28,405,255 |

) | ||||||||||

|

Total

stockholders' equity |

5,074,852

|

517,973

|

(2 |

) |

1,158,822

|

6,751,647

|

|||||||||||||

|

Total

liabilities and stockholders' equity |

$ |

8,742,251 |

$ |

1,667,965 |

$ |

5,512,409 |

$ |

15,922,624 |

|||||||||||

|

NOTES:

|

| (1) | Elimination of Common stock and accumulated earnings of CQ Systems before the acquisition and to record the purchase of CQ Systems by NetSol. The initial purchase price is $6,730,382, of which one-half is due at closing in cash and stock and the remaining half to be paid within one year, and after the price has been adjusted up or down when the audited 3/31/06 numbers are available. No interest is accrued on the balance remaining after closing. |

|

Purchase

Price allocation: |

$ |

||||||

|

Common

Stock, 681,965 shares |

682

|

||||||

|

Additional

paid in capital |

1,676,113

|

||||||

|

Cash

|

700,000

|

||||||

|

Cash,

provided by short-term notes |

1,000,000

|

||||||

|

Notes

payable |

3,353,587

|

||||||

|

Total

purchase price |

6,730,382

|

||||||

|

CQ

equity (net assets and liabilities) |

517,973

|

||||||

|

Intangible

assets: |

|||||||

|

Customer

Lists |

1,316,880

|

||||||

|

Licenses

|

2,190,807

|

||||||

|

Goodwill

|

2,704,722

|

||||||

|

6,212,409

|

6,212,409

|

||||||

|

6,730,382

|

|||||||

|

NETSOL

TECHNOLOGIES INC AND SUBSIDIARIES | ||||||||

|

CONSOLIDATED

PRO-FORMA STATEMENT OF OPERATIONS | ||||||||

|

FOR

THE YEAR ENDED JUNE 30, 2003 | ||||||||

|

(UNAUDITED) |

|

NetSol |

CQ

Systems |

|

|

|

||||||||||||

|

|

as

of 6/30/03 |

as

of 3/31/03 |

Pro

Forma |

|

Pro

Forma |

|||||||||||

|

|

|

(Historical) |

|

(Historical) |

|

Adjustment |

|

|

|

Combined |

||||||

|

Net

Revenue |

$ |

3,745,386 |

$ |

3,821,892 |

$ |

-- |

$ |

7,567,278 |

||||||||

|

Cost

of revenue |

1,778,993

|

1,654,608

|

--

|

3,433,601

|

||||||||||||

|

Gross

profit |

1,966,393

|

2,167,284

|

--

|

4,133,677

|

||||||||||||

|

Operating

expenses |

4,434,643

|

2,013,685

|

701,537

|

(3 |

) |

7,149,862

|

||||||||||

|

Income

(loss) from operations |

(2,468,250 |

) |

153,599

|

(701,537 |

) |

(3,016,185 |

) | |||||||||

|

Other

income and (expenses) |

(147,331 |

) |

(34,560 |

) |

--

|

(181,891 |

) | |||||||||

|

Income

(loss) from continuing operations |

(2,615,581 |

) |

119,039

|

(701,537 |

) |

(3,198,076 |

) | |||||||||

|

Gain

from discontinuation of a subsidiary |

478,075

|

--

|

--

|

478,075

|

||||||||||||

|

Net

income (loss) |

(2,137,506 |

) |

119,039

|

(701,537 |

) |

(2,720,001 |

) | |||||||||

|

Other

comprehensive income (loss): |

||||||||||||||||

|

Translation

adjustment |

(380,978 |

) |

70,997

|

--

|

(309,981 |

) | ||||||||||

|

Comprehensive

income (loss) |

$ |

(2,518,484 |

) |

$ |

190,036 |

$ |

(701,537 |

) |

$ |

(3,029,982 |

) | |||||

|

EARNINGS

PER SHARE |

||||||||||||||||

| Weighted -average number of shares outstanding |

5,194,167

|

100,000

|

5,294,167

|

|||||||||||||

|

Income

(loss) per share |

$ |

(0.41 |

) |

$ |

1.19 |

$ |

(0.51 |

) | ||||||||

|

NOTES: |

| (1) | Loss per share data shown above are applicable for both primary and fully diluted. |

| (2) | Weighted-average number of shares outstanding for the combined entity includes all shares issued for the acquisition of 681,964 as if outstanding as of July 1, 2002. |

| (3) | Amortization of intangible assets acquired in acquisition |

|

NETSOL

TECHNOLOGIES INC AND SUBSIDIARIES | ||||||||

|

CONSOLIDATED

PRO-FORMA STATEMENT OF FINANCIAL CONDITIONS | ||||||||

|

FOR

THE PERIOD ENDED DECEMBER 31, 2004 | ||||||||

|

(UNAUDITED) |

|

NetSol |

CQ

Systems |

|||||||||||||||

|

as

of 12/31/04 |

as

of 12/31/04 |

Pro

Forma |

Pro

Forma |

|||||||||||||

|

(Historical) |

(Historical) |

Adjustment |

Combined |

|||||||||||||

|

ASSETS |

||||||||||||||||

|

Current

Assets |

$ |

5,554,445 |

$ |

2,013,642 |

$ |

(700,000 |

) |

(1 |

) |

$ |

6,868,087 |

|||||

|

Property

& equipment, net |

4,276,307

|

339,527

|

--

|

4,615,834

|

||||||||||||

|

Intangible

assets, net |

4,003,152

|

--

|

5,974,686

|

(1 |

) |

9,977,838

|

||||||||||

|

Total

assets |

$ |

13,833,904 |

$ |

2,353,169 |

$ |

5,274,686 |

$ |

21,461,759 |

||||||||

|

|

||||||||||||||||

|

LIABILITIES

& STOCKHOLDERS' EQUITY |

||||||||||||||||

|

Current

liabilities |

$ |

2,527,728 |

$ |

1,467,228 |

$ |

-- |

$ |

3,994,957 |

||||||||

| Obligations under capitalized leases, less current maturities |

56,910

|

124,803

|

--

|

181,713

|

||||||||||||

|

Deferred

tax |

--

|

5,442

|

--

|

5,442

|

||||||||||||

|

Notes

payable |

--

|

--

|

4,353,587

|

(1 |

) |

4,353,586

|

||||||||||

|

Convertible

debenture |

112,500

|

--

|

--

|

112,500

|

||||||||||||

|

Total

liabilities |

2,697,138

|

1,597,473

|

4,353,587

|

8,648,198

|

||||||||||||

|

Minority

Interest |

99,752

|

--

|

--

|

99,752

|

||||||||||||

|

Stockholders'

equity; |

||||||||||||||||

|

Common

stock |

12,254

|

159,210

|

(158,528 |

) |

(1 |

) |

12,936

|

|||||||||

|

Additional

paid in capital |

43,119,861

|

--

|

1,676,113

|

(1 |

) |

44,795,974

|

||||||||||

|

Common

stock to be issued |

254,800

|

--

|

--

|

254,800

|

||||||||||||

|

Stock

subscription receivable |

(1,375,642 |

) |

--

|

--

|

(1,375,642 |

) | ||||||||||

|

Treasury

stock |

(27,197 |

) |

--

|

--

|

(27,197 |

) | ||||||||||

|

Other

comprehensive income (loss) |

(323,619 |

) |

43,149

|

(43,149 |

) |

(1 |

) |

(323,619 |

) | |||||||

|

Accumulated

earnings (deficit) |

(30,623,443 |

) |

553,337

|

(553,337 |

) |

(1 |

) |

(30,623,443 |

) | |||||||

|

Total

stockholders' equity |

11,037,014

|

755,696

|

921,099

|

12,713,809

|

||||||||||||

|

Total

liabilities and stockholders' equity |

$ |

13,833,904 |

$ |

2,353,169 |

$ |

5,274,686 |

$ |

21,461,759 |

||||||||

|

NOTES:

|

| (1) | Elimination of Common stock and accumulated earnings of CQ Systems before the acquisition and to record the purchase of CQ Systems by NetSol. The initial purchase price is $6,730,382, of which one-half is due at closing in cash and stock and the remaining half to be paid within one year, and after the price has been adjusted up or down when the audited 3/31/06 numbers are available. No interest is accrued on the balance remaining after closing. |

|

Purchase

Price allocation: |

$ |

||||||

|

Common

Stock, 681,965 shares |

682

|

||||||

|

Additional

paid in capital |

1,676,113

|

||||||

|

Cash

|

700,000

|

||||||

|

Cash,

provided by short-term notes |

1,000,000

|

||||||

|

Notes

payable |

3,353,587

|

||||||

|

Total

purchase price |

6,730,382

|

||||||

|

CQ

equity (net assets and liabilities) |

755,696

|

||||||

|

Intangible

assets: |

|||||||

|

Customer

Lists |

1,316,880

|

||||||

|

Licenses

|

2,190,807

|

||||||

|

Goodwill

|

2,466,999

|

||||||

|

5,974,686

|

5,974,686

|

||||||

|

6,730,382

|

|||||||

|

NETSOL

TECHNOLOGIES INC AND SUBSIDIARIES | ||||||||

|

CONSOLIDATED

PRO-FORMA STATEMENT OF OPERATIONS | ||||||||

|

FOR

THE PERIOD ENDED DECEMBER 31, 2004 | ||||||||

|

(UNAUDITED) |

|

NetSol |

CQ

Systems |

|

|

|

||||||||||||

|

|

as

of 12/31/04 |

as

of 12/31/04 |

Pro

Forma |

|

Pro

Forma |

|||||||||||

|

|

|

(Historical) |

|

(Historical) |

|

Adjustment |

|

|

|

Combined |

||||||

|

Net

Revenue |

$ |

4,781,532 |

$ |

2,485,266 |

$ |

-- |

$ |

7,266,798 |

||||||||

|

Cost

of revenue |

1,580,620

|

1,550,006

|

--

|

3,130,626

|

||||||||||||

|

Gross

profit |

3,200,912

|

935,260

|

--

|

4,136,172

|

||||||||||||

|

Operating

expenses |

2,757,165

|

833,863

|

350,769

|

(3 |

) |

3,941,794

|

||||||||||

|

Income

(loss) from operations |

443,747

|

101,397

|

(350,769 |

) |

194,378

|

|||||||||||

|

Other

income and (expenses) |

(379,314 |

) |

6,782

|

--

|

(372,532 |

) | ||||||||||

|

Income

(loss) from continuing operations |

64,433

|

108,179

|

(350,769 |

) |

(178,154 |

) | ||||||||||

|

Minority

interest in subsidiary |

14,259

|

--

|

--

|

14,259

|

||||||||||||

|

Net

income (loss) |

78,692

|

108,179

|

(350,769 |

) |

(163,895 |

) | ||||||||||

|

Other

comprehensive income (loss): |

||||||||||||||||

|

Translation

adjustment |

(173,409 |

) |

(95,635 |

) |

--

|

(269,044 |

) | |||||||||

|

Comprehensive

income (loss) |

$ |

(94,717 |

) |

$ |

12,544 |

$ |

(350,769 |

) |

$ |

(432,939 |

) | |||||

|

EARNINGS

PER SHARE |

||||||||||||||||

| Weighted -average number of shares outstanding |

10,755,918

|

100,000

|

10,855,918

|

|||||||||||||

|

Income

(loss) per share |

$ |

0.01 |

$ |

1.08 |

$ |

(0.02 |

) | |||||||||

|

NOTES: |

| (1) | Loss per share data shown above are applicable for primary |

| (2) | Weighted-average number of shares outstanding for the combined entity includes all shares issued for the acquisition of 681,964 shares as if outstanding as of July 1, 2003. |

| (3) | Amortization of intangible assets acquired in acquisition |

|

2004 |

2003 |

||||||

|

Netsol

USA |

$ |

676,857 |

$ |

508,868 |

|||

|

Netsol

Tech (1) |

3,190,049

|

1,315,413

|

|||||

|

Netsol

Private |

483,788

|

265,599

|

|||||

|

Netsol

Connect |

778,598

|

1,185,162

|

|||||

|

Netsol

UK |

356,215

|

83,737

|

|||||

|

Netsol-Abraxas

Australia |

263,555

|

386,607

|

|||||

|

Total

Net Revenues |

$ |

5,749,062 |

$ |

3,745,386 |

|||

| (1) |

Refers

to NetSol Technologies (Pvt.) Limited |

|

2005 |

2004 |

||||||||||||

|

Netsol

USA |

$ |

21,606 |

0.68 |

% |

$ |

274,368 |

16.13 |

% | |||||

|

Netsol

Tech |

1,623,307

|

50.87 |

% |

884,772

|

52.02 |

% | |||||||

|

Netsol

Private |

95,367

|

2.99 |

% |

176,969

|

10.41 |

% | |||||||

|

Netsol

Connect |

294,420

|

9.23 |

% |

202,130

|

11.88 |

% | |||||||

|

Netsol

UK |

125,782

|

3.94 |

% |

93,089

|

5.47 |

% | |||||||

|

Netsol-Abraxas

Australia |

76,629

|

2.40 |

% |

69,446

|

4.08 |

% | |||||||

|

CQ

Systems |

799,761

|

25.06 |

% |

--

|

0.00 |

% | |||||||

|

NetSol

- TiG |

154,046

|

4.83 |

% |

--

|

0.00 |

% | |||||||

|

Total

Net Revenues |

$ |

3,190,918 |

100.00 |

% |

$ |

1,700,774 |

100.00 |

% | |||||

|

2005 |

2004 |

||||||||||||

|

Netsol

USA |

$ |

295,725 |

3.71 |

% |

$ |

481,868 |

12.41 |

% | |||||

|

Netsol

Tech |

4,564,167

|

57.25 |

% |

2,136,968

|

55.05 |

% | |||||||

|

Netsol

Private |

562,872

|

7.06 |

% |

272,650

|

7.02 |

% | |||||||

|

Netsol

Connect |

852,640

|

10.69 |

% |

503,530

|

12.97 |

% | |||||||

|

Netsol

UK |

574,849

|

7.21 |

% |

274,786

|

7.08 |

% | |||||||

|

Netsol-Abraxas

Australia |

168,390

|

2.11 |

% |

211,929

|

5.46 |

% | |||||||

|

CQ

Systems |

799,761

|

10.03 |

% |

--

|

0.00 |

% | |||||||

|

NetSol

- TiG |

154,046

|

1.93 |

% |

--

|

0.00 |

% | |||||||

|

Total

Net Revenues |

$ |

7,972,450 |

100.00 |

% |

$ |

3,881,731 |

100.00 |

% | |||||

| · |

Injection

of additional new capital of up to $500,000 in a strategic joint-venture

of NetSol-TiG. This partnership serves to outsource TiG’s software

development business to our offshore-based development facility.

|

| · |

The

final payment to former CQ Systems shareholders of the remaining

consideration. The amount due is based on the earnings of CQ Systems

during the period of March 31, 2005 to March 31, 2006 and will be paid in

cash, equity or a combination of both. The initial consideration, which

was based on revenues for the period ending March 31, 2005, total

approximately $3.5 million and was paid in cash and restricted shares of

common stock. While the agreement permits the final consideration to be

paid, in part, in restricted shares of common stock, management believes

that improving net cash position of CQ and Company strongly improves the

potential of meeting this obligation without raising new capital.

|

| · |

New

capital requirement for NetSol Akhter, the telecom division in an amount

up to $2.0 million as required by the agreement with

Akhter. |

| · |

Working

capital of $1.0 million for debts payments, new business development

activities and infrastructure

enhancements. |

| · |

Final

note payments of $875,000 due in 12 months that was received from three

separate investors to close the CQ acquisition in February 2005. These

investors, who have long standing relationships with the Company, permit

the extension of the maturity date upon the agreement of these investors.

|

| · |

Stock

volatility due to market conditions in general and NetSol stock

performance in particular. This may cause a shift in our approach to raise

new capital through other sources such as secured long term

debt. |

| · |

Analysis

of the cost of raising capital in the U.S., Europe or emerging markets. By

way of example only, if the cost of raising capital is high in one market

and it may negatively affect the company’s stock performance, we may

explore options available in other markets.

|

|

Location/Approximate

Square Feet |

Purpose/Use |

Monthly

Rental Expense |

||||||||

|

Australia |

1,140 |

Computer

and General Office |

$ |

1,380 |

||||||

|

United

Kingdom |

378 |

General

Office |

$ |

5,500 |

||||||

|

Maryland |

1,380 |

General

Office |

$ |

2,530 |

||||||

|

2002-03 |

2003-04 |

2004-05 |

|||||||||||||||||

|

High |

Low |

High |

Low |

High |

Low |

||||||||||||||

|

1st

(ended September 30) |

.80 |

.35 |

5.50 |

1.94 |

1.99 |

1.09 |

|||||||||||||

|

2nd

(ended December 31) |

1.30 |

.25 |

3.16 |

2.05 |

2.71 |

1.14 |

|||||||||||||

|

3rd

(ended March 31) |

1.24 |

.75 |

3.15 |

2.07 |

2.67 |

1.82 |

|||||||||||||

|

4th

(ended June 30) |

3.50 |

.95 |

3.09 |

2.01 |

----- |

---- |

|||||||||||||

|

Long

Term Compensation |

||||||||||||||||

| Long Term | ||||||||||||||||

| Compensation | ||||||||||||||||

|

Awards

(2) |

Securities | |||||||||||||||

| Restricted |

Underlying |

|||||||||||||||

| Fiscal Year |

Annual

Compensation(1) |

Stock |

Options/ |

|||||||||||||

|

Name

and Principal Position |

Ended |

Salary |

Bonus |

Awards(3) |

SARs

(4) |

|||||||||||

|

Najeeb

U. Ghauri, Chief Financial Officer, Chairman,

Director |

2004 |

$ |

200,000 |

-0- |

-0- |

50,000(5 |

) | |||||||||

|

50,000(6 |

) | |||||||||||||||

|

25,000(7 |

) | |||||||||||||||

|

20,000(8 |

) | |||||||||||||||

|

30,000(9 |

) | |||||||||||||||

|

2003 |

$ |

120,000 |

-0- |

-0- |

-0- |

|||||||||||

|

2002 |

$ |

100,000 |

-0- |

-0- |

85,000(10 |

) | ||||||||||

|

100,000(11 |

) | |||||||||||||||

|

20,000(12 |

) | |||||||||||||||

|

Naeem

Ghauri, CEO, Director |

2004 |

$ |

207,900(13 |

) |

-0- |

-0- |

50,000(5 |

) | ||||||||

|

50,000(6 |

) | |||||||||||||||

|

25,000(7 |

) | |||||||||||||||

|

20,000(8 |

) | |||||||||||||||

|

30,000(9 |

) | |||||||||||||||

|

2003 |

$ |

125,000 |

-0- |

-0- |

-0- |

|||||||||||

|

2002 |

$ |

100,000 |

-0- |

-0- |

70,000(14 |

) | ||||||||||

|

100,000(11 |

) | |||||||||||||||

|

20,000(12 |

) | |||||||||||||||

|

Salim

Ghauri, President, Director |

2004 |

$ |

110,000 |

-0- |

-0- |

50,000(5 |

) | |||||||||

|

50,000(6 |

) | |||||||||||||||

|

25,000(7)- |

||||||||||||||||

|

20,000(8 |

) | |||||||||||||||

|

30,000(9 |

) | |||||||||||||||

|

2003 |

$ |

100,000 |

-0- |

-0- |

-0- |

|||||||||||

|

2002 |

$ |

100,000 |

-0- |

-0- |

70,000(14 |

) | ||||||||||

|

100,000(11 |

) | |||||||||||||||

|

20,000(12 |

) | |||||||||||||||

|

Patti

L. W. McGlasson, Secretary, Corporate

Counsel |

2004 |

$ |

82,000 |

-0- |

5,000(15 |

) |

5,000(16 |

) | ||||||||

|

5,000(17 |

) | |||||||||||||||

|

20,000(8 |

) | |||||||||||||||

|

30,000(9 |

) | |||||||||||||||

| (1) | No officers received any bonus or other annual compensation other than salaries during fiscal 2004 or any benefits other than those available to all other employees that are required to be disclosed. These amounts are not inclusive of automobile allowances, where applicable. |

| (2) | No officers received any long-term incentive plan (LTIP) payouts or other payouts during fiscal years 2004, 2003 or 2002. |

| (3) | All stock awards are shares of our Common Stock. |

| (4) | All securities underlying options are shares of our Common Stock. We have not granted any stock appreciation rights. No options were granted to the named executive officers in fiscal year 2003. Options are reflected in post-reverse split numbers. All options are currently exercisable or may be exercised within sixty (60) days of the date of this prospectus and are fully vested. |

| (5) | Includes options to purchase 50,000 shares of our common stock granted on January 1, 2004 at the exercise price of $2.21 per share. These options must be exercised within five years after the grant date. |

| (6) | Includes options to purchase 50,000 shares of our common stock granted on January 1, 2004 at the exercise price of $3.75 per share. These options must be exercised within five years after the grant date. |

| (7) | Includes options to purchase 12,500 shares of our common stock at $5.00 per share. These options must be exercised within five years after the grant date. |

| (8) | Includes options to purchase 20,000 shares of our common stock at $2.65 per share. These options must be exercised within five years after the grant date. |

| (9) | Includes options to purchase 30,000 shares of our common stock at $5.00 per share. These options must be exercised within five years after the grant date. |

| (10) | Includes options to purchase 85,000 shares of our common stock granted on February 16, 2002 at the exercise price of $.75 per share. Options must be exercised within five years after the grant date. |

| (11) | Includes options to purchase 100,000 shares of our common stock granted on February 16, 2002 at the exercise price of $1.25 per share. |

| (12) | Includes options to purchase 200,000 shares of our common stock granted on February 16, 2002 at the exercise price of $2.50 per share. |

| (13) | Mr. Ghauri salary is 110,000 British Pounds Sterling. The total in this table reflects a conversion rate of 1.89 dollars per pound. |

| (14) | Includes options to purchase 70,000 shares of our common stock granted on February 16, 2002 at the exercise price of $.75 per share. Options must be exercised within five years after the grant date. |

| (15) | In May 2004, Ms. McGlasson received 5,000 shares of common stock as a performance bonus arising out of her services as counsel for the Company. |

| (16) | Includes options to purchase 5,000 shares of common stock at the exercise price of the lesser of the $2.30 or the market price of the shares on the date of exercise less $2.00. |

| (17) | Includes options to purchase 5,000 shares of common stock at the exercise price of $3.00 per share. |

|

Name |

Shares

Acquired on Exercise (#) |

Value

Realized (1) ($) |

Number

of Unexercised Options/SARs at fiscal year end (##) Exercisable (2) /

Unexercisable |

Value

of unexercised in-the-money at fiscal year end ($)Exercisable (2) /

Unexercisable |

|||||||||

|

Najeeb

Ghauri, CFO , Director , Chairman |

87,223 |

$ |

0.00 |

150,000/150,000 |

$ |

2,000/$0.00 |

|||||||

|

Salim

Ghauri, President, Director |

67,777 |

$ |

0.00 |

155,000/155,000 |

$ |

2,000/$0.00 |

|||||||

|

Naeem

Ghauri, CEO, Director |

51,557 |

$ |

0.00 |

1500,000/155,000 |

$ |

$2,000/$0.00 |

|||||||

|

Patti

L. W. McGlasson, Secretary

Corporate

Counsel |

2,500 |

$ |

0.00 |

60,000/10,000 |

$ |

525/$1,050 |

|||||||

| (1) |

The

closing price of the stock at the June 30, 2004, Fiscal Year End was

$2.21. |

| (2) |

All

options are currently exercisable. |

NETSOL TECHNOLOGIES, INC. AND SUBSIDIARIES

INDEX TO CONSOLIDATED FINANCIAL STATEMENTS

Description Page

- ----------- ----

Report of Independent Registered Public Accounting Firm..............................................F-2

Auditor's Report to the Members......................................................................F-3

Consolidated Balance Sheet as of June 30, 2004 (restated)............................................F-6

Consolidated Statements of Operations for the Years Ended June 30, 2004 (restated) and 2003..........F-4

Consolidated Statements of Stockholders' Equity for the Years Ended

June 30, 2004 (restated) and 2003..................................................................F-5

Consolidated Statements of Cash Flows for the Years Ended June 30, 2004 (restated) and 2003..........F-7

Notes to Consolidated Financial Statements...........................................................F-9

F-1

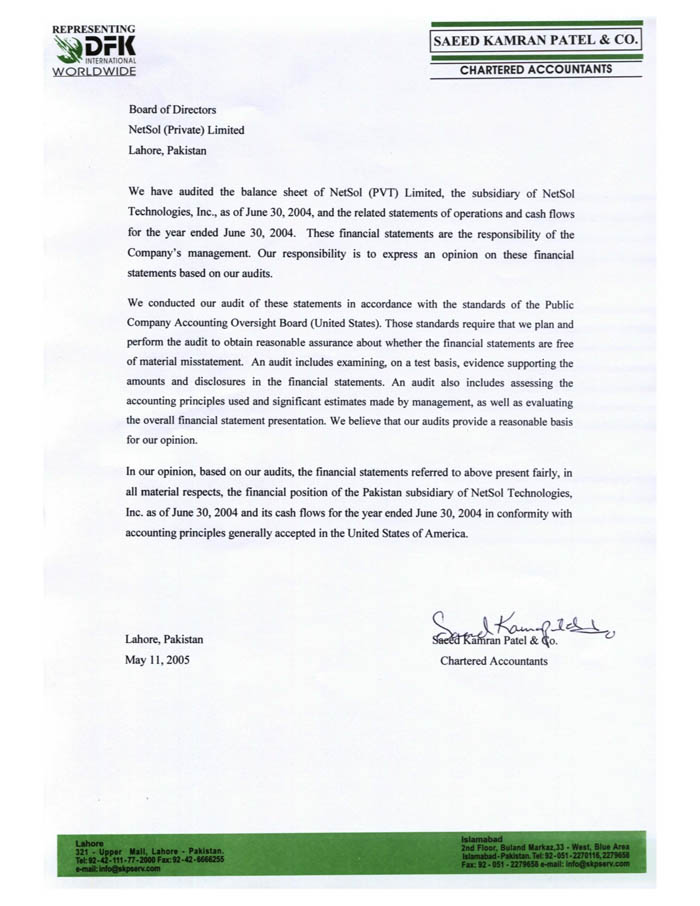

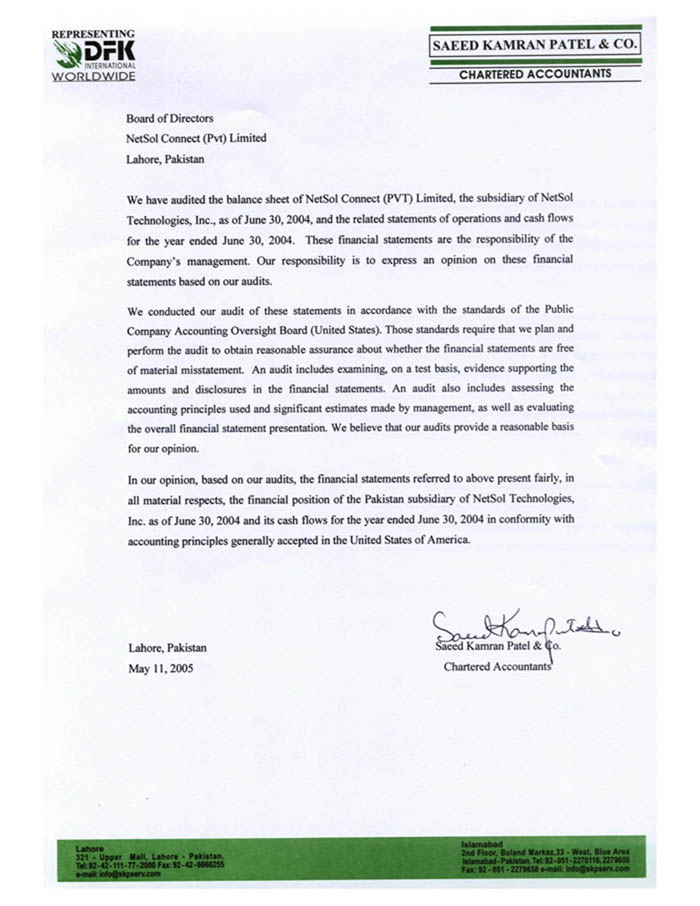

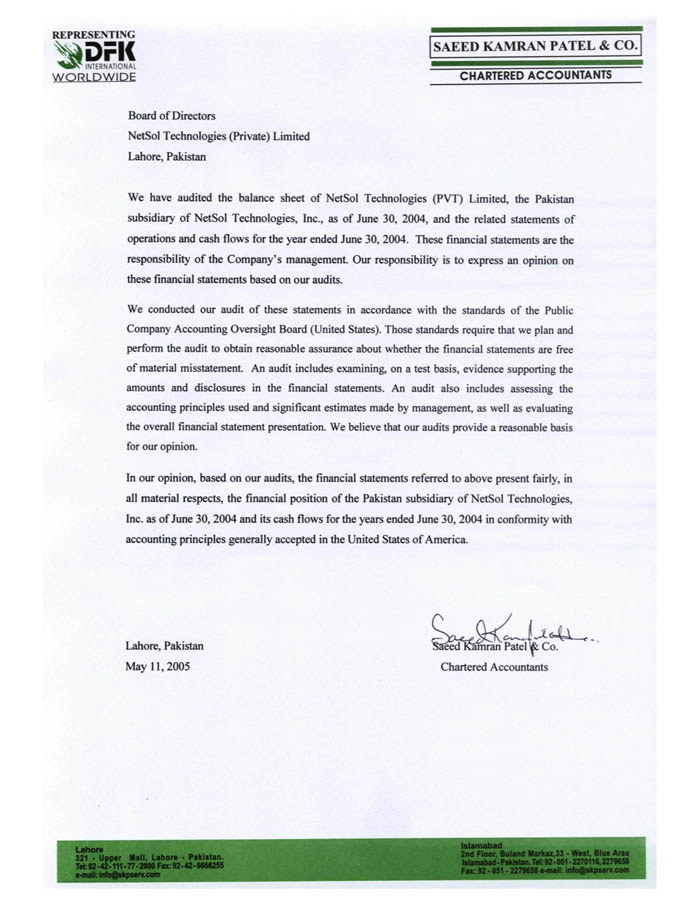

REPORT OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM

Board of Directors

NetSol Technologies, Inc. and subsidiaries

Calabasas, California

We have audited the accompanying consolidated balance sheet of NetSol

Technologies, Inc. and subsidiaries as of June 30, 2004, and the related

consolidated statements of operations, stockholders' equity and cash flows for

the years ended June 30, 2004 and 2003. These financial statements are the

responsibility of the Company's management. Our responsibility is to express an

opinion on these consolidated financial statements based on our audits. We did

not audit the financial statements of Network Technologies (PVT) Limited, NetSol

(PVT) Limited and NetSol Connect (PVT) Limited,, whose statements reflect

combined total assets of approximately $7,173,282 as of June 30, 2004 and

combined total net revenues of $4,452,435and $2,766,174 for the years ended June

30, 2004 and 2003, respectively. Those statements were audited by other auditors

whose reports have been furnished to us, and in our opinion, insofar as it

relates to the amounts included for Network Technologies (PVT) Limited, NetSol

(PVT) Limited and NetSol Connect (PVT) Limited, for the years ended June 30,

2004 and 2003, is based solely on the report of the other auditors.

We conducted our audit of these statements in accordance with the standards of

the Public Company Accounting Oversight Board (United States). Those standards

require that we plan and perform the audit to obtain reasonable assurance about

whether the financial statements are free of material misstatement. An audit

includes examining, on a test basis, evidence supporting the amounts and

disclosures in the financial statements. An audit also includes assessing the

accounting principles used and significant estimates made by management, as well

as evaluating the overall financial statement presentation. We believe that our

audit and the report of the other auditors provide a reasonable basis for our

opinion.

In our opinion, based on our audits and the reports of other auditors, the

consolidated financial statements referred to above present fairly, in all

material respects, the consolidated financial position of NetSol Technologies,